The Quiet Math Behind Every Retail Energy Contract

A look inside the pricing decisions that shape every retail energy contract, for the people writing and selling them and the people signing them.

Geno J. Cortina

5/8/2026

Most energy buyers, and a fair number of brokers, evaluate retail electricity offers the same way they evaluate most commodity purchases. They look at the headline price, compare it across suppliers, and pick the most competitive number. It's a reasonable instinct. It's also the single biggest reason customers end up surprised by their bills, frustrated with their supplier, and skeptical of the broker who placed them.

The contract price is not the deal. The treatment of the components inside the price is the deal.

Every retail electricity price is built up from a stack of cost components: energy, capacity, transmission, ancillaries, line losses, RECs, taxes, and a handful of others depending on the market. Each of those components can be treated one of three ways in the contract: fixed, fixed subject to adjustment, or passed through. Two suppliers can quote nearly identical headline prices and deliver dramatically different economics over the term of the contract, simply because they treated the components differently. Understanding those differences is the difference between a contract that performs the way you expected and a contract that doesn't.

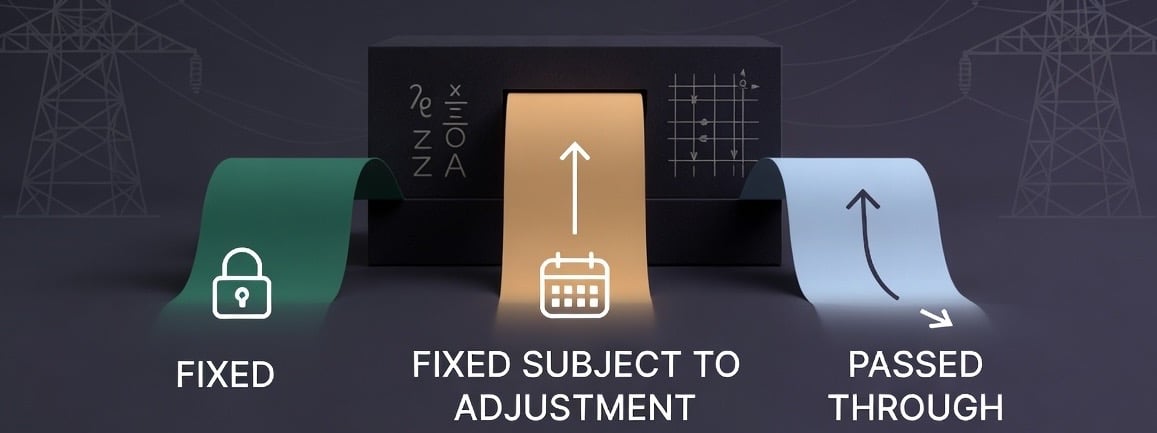

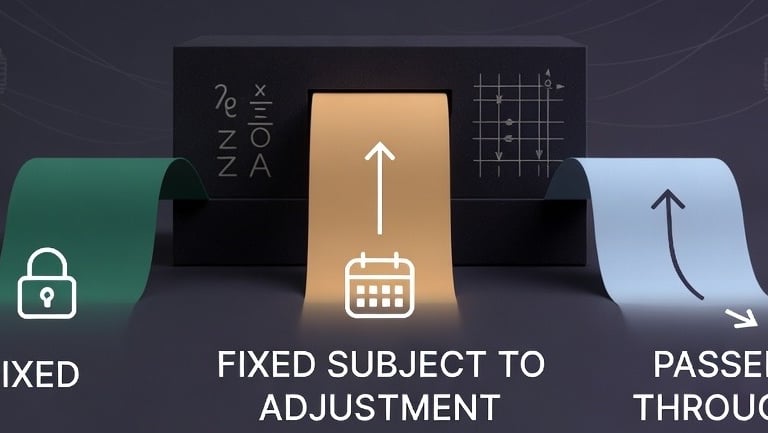

The Three Treatments

Fixed means exactly what it sounds like. The supplier has priced the component into the all-in rate and is taking the risk on what the actual cost turns out to be. If the underlying cost rises during the term, the supplier absorbs it. If it falls, the supplier keeps the upside. The customer pays the contracted rate regardless. Fixed treatment offers the customer maximum predictability and shifts the risk to the supplier, which the supplier, in turn, prices for.

Fixed subject to adjustment is the most misunderstood treatment of the three, and it's where the most expectation gaps occur. The component is presented as a fixed number in the offer and the contract, but the contract language allows the supplier to adjust the rate when certain conditions are met. The most common trigger is the finalization of an underlying cost after the contract is signed. Capacity in PJM is the classic example. RTO capacity auctions clear on a schedule that doesn't align with most contract sign dates, so suppliers have to put a placeholder rate in the price for delivery years where the auction hasn't yet cleared. Different suppliers handle this differently. Some price the placeholder at the auction offer cap to protect themselves on the upside. Others use the floor to win the deal and adjust later. Others use an average or a forecast. When the actual auction clears, the rate gets adjusted to reflect the cleared price, and the customer's bill reflects the difference. The customer who didn't read the contract language carefully thinks they bought a fixed price. The supplier knows they didn't.

Passed through means the component is not embedded in the headline rate at all. The customer pays the actual cost, as it's incurred, on top of the energy rate. There's no markup baked in, no risk premium, no surprise adjustment. Just the actual cost flowing through to the bill, typically with some level of detail showing how it was calculated. Pass-through treatment offers the customer the lowest headline rate and the most transparency on what they're actually paying for, but it also means accepting cost variability over the term.

Each treatment has a legitimate use case. None of them is inherently better than the others. The problem isn't the treatment. It's the mismatch between how the component is treated in the contract and what the customer thinks they bought.

Capacity: The Component That Trips Everyone Up

Capacity is the canonical example because it shows up in almost every PJM, NYISO and ISO-NE contract and because the auction timing creates structural ambiguity that suppliers handle very differently.

Consider three suppliers quoting a three-year fixed-price contract starting June of next year. The first delivery year's capacity has cleared, so everyone is working off the same number for that period. The second and third delivery years haven't cleared yet, so each supplier has to make a pricing decision.

Supplier A prices both unsettled years at the offer cap, the maximum the auction can clear at. Their headline rate is the highest of the three. If you sign with them and the auctions clear lower than the cap, you've overpaid.

Supplier B prices both unsettled years at the floor. Their headline rate is the lowest of the three. If you sign with them and the auctions clear above the floor (which they usually do), the contract gets adjusted upward when the auctions clear, and you end up paying meaningfully more than the rate you saw in the offer.

Supplier C uses a forecast or a structured average. Their headline rate sits in the middle. The adjustment when the auctions clear is smaller in either direction.

All three suppliers are quoting a "fixed price" contract. All three are technically telling the truth in their contracts & marketing materials. But the customer experience over the life of these three contracts is meaningfully different, and the customer who picked Supplier B because their price was lowest is the customer who is going to be on the phone with their broker in eighteen months, asking why their bill doesn't match the contract they signed.

The fix is not complicated. It's reading the contract language. It's asking the supplier directly how they've treated capacity in the unsettled years and what triggers an adjustment. It's understanding that "fixed subject to adjustment" is not the same as "fixed," and that a competitive headline rate hiding an aggressive adjustment mechanism is not a competitive deal.

The Other Components Worth Knowing

Capacity is the most visible example, but it's far from the only one. Any component with cost volatility or settlement timing that doesn't align with the contract term is a candidate for differential treatment.

Capacity tags and transmission tags deserve their own attention, separate from the underlying capacity and transmission rates. A customer's capacity obligation and network service peak load contribution are recalculated annually based on usage during peak hours from the prior year. When those tags change, and they almost always do, the dollar impact on the contract can be significant, even if the underlying capacity or transmission rates haven't moved at all. Some suppliers fix the tags at contract sign and absorb the risk of changes during the term. Others pass through the cost impact of any tag change, sometimes with a stated tolerance band, sometimes with no tolerance at all. Two contracts at the same headline rate, one with fixed tags and one with pass-through tag adjustments, can deliver materially different economics if the customer's load profile shifts. This is one of the most overlooked sources of post-signing surprises in mid-market and large C&I contracts.

Transmission charges more broadly (network integration service, ancillary transmission costs, and the various FERC-jurisdictional uplifts) are often treated as fixed subject to adjustment because the underlying tariffs are revised annually by the transmission owner. Suppliers who fix these charges fully take the risk on tariff changes. Suppliers who pass them through don't. Suppliers in the middle adjust on a defined trigger.

Ancillary services such as regulation, reserves, and frequency response are typically smaller dollars but more volatile. Different suppliers treat them differently, and the difference can matter at scale.

Line losses vary by utility and zone and can be either embedded in the energy rate or treated as a separate component with its own treatment. Suppliers who embed it in a fixed rate and get the loss factor wrong eat the difference. Suppliers who pass it through don't.

Renewable Energy Credits, where required, are often fixed at contract sign, but the underlying market for RECs can move significantly over a multi-year term, and some suppliers reserve the right to adjust REC charges if compliance costs change materially.

Taxes and regulatory fees are almost always passed through, but the level of detail provided to the customer on the bill, and the timing of when changes flow through, varies meaningfully supplier to supplier.

Capacity-related charges beyond the auction itself, including Reliability Pricing Model adjustments, FRR contributions, and capacity performance penalties in certain markets, can be treated as fixed, adjustable, or passed through. Most customers have no idea these line items exist until they show up on a bill.

The point is not that buyers need to become experts in every one of these components. The point is that buyers need to understand which components their supplier has treated as fixed, which as fixed subject to adjustment, and which as pass-through. They need contract language that's specific enough to hold the supplier to the treatment that was sold.

Adders on Index Products: Where Apples-to-Apples Comparisons Quietly Break Down

The component treatment problem doesn't disappear when you move from fixed-price products to index or block-and-index structures. If anything, it gets harder to see. Buyers and brokers comparing index deals tend to focus on the adder, the supplier's margin and risk premium layered on top of the underlying index, and assume that the lowest adder wins. It's the same headline-price instinct, just translated into a different product structure, and it suffers from the same flaw.

Adders are not standardized. Two suppliers can quote nearly identical adders on the same index product and deliver meaningfully different economics, because what's included in the adder varies supplier to supplier.

The full list of costs that may or may not live inside the adder is longer than most buyers realize. Ancillary services. Capacity scheduling and bidding costs. Congestion management. The supplier's cost of providing collateral. REC compliance for index portions of hybrid products. Balancing or imbalance costs. Each of these can be embedded in a higher adder or passed through separately. Neither approach is wrong. But comparing adders without understanding what's inside them is not actually comparing the deals.

The right question on any index offer is not "what's the adder." It's "what's in the adder, and what's passed through separately." A supplier who can answer that question clearly, in writing, is a supplier worth taking seriously. A supplier who can't, or won't, is a supplier whose bill is going to surprise you.

Credit Treatments: The Other Half of the Pricing Conversation

Component treatment isn't only about costs. It's also about credits, the financial allocations and adjustments that should, in principle, flow back to the customer who's paying for the load.

Deration is the cleanest illustration of how credits get treated differently across suppliers. In PJM and similar markets, a customer's metered load is grossed up to a settlement value at the wholesale node to account for transmission and distribution losses. The deration adjustment then reduces what the customer is charged at that node, effectively passing the loss-factor benefit back to load. For index products, this shows up as a credit. Some suppliers pass the full benefit through to the customer transparently. Others retain part of it inside their adder, presenting a more competitive headline number while keeping a portion of the deration value as supplier margin. The customer comparing two adders in isolation has no way to see the difference. The customer who asks how deration is treated does.

Auction Revenue Rights are the most significant credit instrument in PJM. ARRs are allocated annually to load-serving entities based on historical peak load and represent the right to receive a share of the revenue from the FTR auction. For a customer of meaningful size, the ARR allocation tied to their load can be a real number. But how that value flows back to the customer, if at all, is entirely a matter of contract treatment. Some suppliers credit the ARR value back to the customer explicitly, either as a line-item credit on the bill or as a reduction in the energy rate. Others retain the value entirely as supplier margin and don't disclose it. Others split it on a defined formula. Customers who don't ask about ARR treatment in the contracting process generally don't get the credit, and most don't realize what they've left on the table.

Marginal Loss Credits are similar in spirit. PJM's marginal loss surplus allocation distributes a share of the over-collection from marginal loss pricing back to load. Like ARRs, MLCs can be material at scale. Like ARRs, treatment varies. Some suppliers pass them through to the customer, some keep them, some negotiate a split. And like ARRs, customers generally don't think to ask.

Congestion Revenue Rights, Financial Transmission Rights, and the various market-specific equivalents in other ISOs work on the same principle. A financial right tied to load that has real economic value, treated differently by different suppliers, almost never raised by the customer or the broker during the contracting conversation, and almost always retained as supplier margin by default.

The pattern is consistent across all of these credit instruments. They exist. They have real value. They're tied to the customer's load. The default supplier behavior is to retain the value silently. And the customer who would have benefited from the credit doesn't know to ask, because the cost-side conversation dominates the negotiation.

For sophisticated buyers, especially at meaningful scale, credit treatment can be every bit as material to the all-in economics of a deal as cost treatment. A contract with aggressive cost pass-throughs that also retains all the credit value is structurally lopsided in the supplier's favor in a way that doesn't show up in any headline number. The fix, again, is contract language. Identify the credits that apply in the relevant market. Define the treatment. Specify the methodology. And don't sign a contract that's silent on the credit side, because silence is not neutrality. Silence is the supplier keeping the credits.

What Good Looks Like

A well-structured retail energy contract makes the component treatment explicit. Each major component is identified. The treatment is named. The trigger conditions for any adjustment are defined. The methodology for calculating the adjustment is documented. The level of detail provided to the customer on the bill is specified. There are no surprises because there's nothing left to surprise.

A poorly structured contract obscures the treatment behind ambiguous language, lets the supplier exercise discretion over when and how to adjust, and gives the customer no real recourse when the bill doesn't match the offer. Customers who sign these contracts aren't buying electricity. They're buying optionality that they don't realize they've sold to the supplier.

For brokers, the implication is straightforward. Comparing headline prices across suppliers without comparing component treatments is malpractice. The customer who saved a tenth of a cent on a headline rate and got hit with a five-figure capacity adjustment is not a customer who's coming back, and not a customer who's recommending the broker to anyone else.

For suppliers, the implication is just as clear. The suppliers who win sustainably in this market are the ones who price components honestly, document treatments cleanly, and communicate them clearly to customers and channel partners. The suppliers who win by hiding aggressive treatments behind competitive headline rates win the deal and lose the relationship.

For buyers, the implication is the most important of the three. The headline price is a starting point, not a conclusion. Ask how each component is treated. Ask what triggers an adjustment. Ask how the adjustment is calculated. Ask how credits are handled. Ask to see the contract language, not the marketing material. And if the answers aren't clear, that's the answer.

The goal of a retail energy contract isn't to win the lowest headline rate. It's to make sure the price you signed is the price you pay, that the credits you're entitled to actually reach you, and that the bill at the end of the month matches the deal at the beginning of the term. Component treatment, on both sides of the ledger, is where that promise either holds up or falls apart.

Crocevia Advisors works across the retail energy market: helping suppliers design products and pricing structures that hold up to scrutiny, helping brokers evaluate offers and protect their customers, and helping end-use customers understand what they're actually signing. Clear component treatment, clean contract language, and the operational alignment to deliver what was sold.

Take the next step.

Contact Crocevia Advisors for a confidential conversation. Visit croceviaadvisors.com or reach out directly to gcortina@croceviaadvisors.com.

Crocevia Advisors – Clarity at the Crossroads. Advantage in the Markets.

Stay informed

Receive tailored insights and updates from our team

Let's have a conversation

Contact us for bespoke commercial advisory

Get in touch

Contact Us

+1-201-364-9955

Follow Us:

© 2026. Crocevia Advisors LLC All rights reserved.